The Critical Role of Timely Invoicing in Cash Flow Management

In today’s fast-paced business environment, maintaining a healthy cash flow is paramount for the sustainability and growth of small to medium-sized enterprises (SMEs). One fundamental aspect that significantly influences cash flow is the efficiency of your invoicing process. Timely invoicing, coupled with accuracy, ensuring businesses can meet their financial obligations, seize growth opportunities, and maintain a robust financial base. In this discussion, we delve into the significance of getting sales invoices out on time and explore strategies to enhance your invoicing process for better cash flow management.

The Importance of Timely Invoicing

Timely invoicing is not just about sending out bills – it’s about setting the pace for your business’s cash flow. When invoices are dispatched promptly following the delivery of goods or services, it triggers the start of the payment cycle, reducing the time it takes for funds to enter your business. This immediate action helps maintain a steady stream of income, ensuring that your business can cover operational costs, such as payroll and other overheads, without unnecessary delays.

Likewise, issuing invoices right after services have been rendered capitalises on the client’s fresh satisfaction, potentially leading to quicker payments. It reflects a professional approach to business, reinforcing trust between you and your clients.

Enhancing Cash Flow Through Efficient Invoicing

An efficient invoicing process is instrumental in enhancing your business’s cash flow. Here are several strategies to ensure that your invoicing contributes positively to your cash flow management:

- Automate the Invoicing Process: Utilise invoicing software to automate your billing process. Automation ensures invoices are generated and sent out immediately upon completion of a service or sale. This not only saves time but also minimises human error, ensuring accuracy in your invoices.

- Set Clear Payment Terms: Clearly state your payment terms on every invoice. Include due dates, acceptable payment methods, and any late payment fees. Transparent communication of payment expectations sets a professional tone and reduces the likelihood of delayed payments.

- Offer Multiple Payment Methods: By providing various payment options, such as bank transfers, credit cards, and online payment platforms, you make it convenient for clients to settle their invoices promptly.

- Early Payment Incentives: Consider offering discounts or other incentives for early payments. This can encourage clients to pay sooner, improving your cash flow.

- Regular Follow-ups: Establish a routine for following up on outstanding invoices. Gentle reminders before the due date can keep your invoice at the top of your client’s mind, while polite follow-ups post-due date can prompt immediate action without harming the business relationship.

The Impact of Timely Invoicing on Business Growth

Timely invoicing plays a crucial role in not just maintaining but also growing your business. With an efficient cash flow, you are better positioned to invest in marketing, new product and service development, or expansion efforts. It provides the financial flexibility to take advantage of market opportunities as they arise, whether that’s a bulk purchase discount from a supplier or the chance to expand into new markets.

Furthermore, the efficiency of your invoicing process can be a competitive advantage. In industries where late invoicing is common, being the business that consistently invoices and follows up professionally can set you apart, leading to stronger client relationships and more referral business.

In conclusion, timely invoicing is much more than a clerical task. It’s a strategic business activity that directly impacts your cash flow management. By ensuring that invoices are sent out promptly and accurately, you can maintain a healthy cash flow, which is the lifeline of your business. Implementing the strategies outlined above will not only improve your cash flow but also enhance your business’s overall financial health, allowing you to achieve your growth objectives and build lasting relationships with your clients.

Remember, effective cash flow management starts with your invoicing process. By prioritising timely invoicing, you’re not just chasing payments, but building the foundation for a successful and sustainable business. At Cloudit Bookkeeping, we understand the challenges SMEs face in managing their finances. Our suite of services is designed to help you streamline your financial operations, including optimising your invoicing process, so you can focus on what you do best – growing your business. Get in touch to find out how we can help.

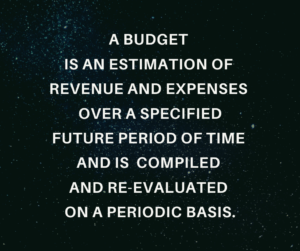

Budget for Business:

Budget for Business: